Mortgage Laddering: How to Optimise Your Home Loan by Splitting into Multiple Parts

Nov 4, 2025

Want more flexibility and less refinancing risk? Discover how mortgage laddering (splitting your home loan into parts) can help you manage interest rate changes and save on your mortgage.

The Smarter Way to Manage Your Mortgage

Interest rates in New Zealand have been anything but stable over the past few years — and for borrowers, timing your mortgage structure can feel like a gamble. Fix for five years and you risk missing future rate drops; float entirely and you’re exposed if rates climb again.

That’s where mortgage laddering comes in and you can use our handy mortgage laddering simulator to calculate your own scenarios and understand the impact.

This strategy lets you divide your home loan into multiple parts (each with different terms or rate types) to balance risk, capture flexibility, and smooth out the impact of market swings. It’s a concept borrowed from term deposits — but applied to mortgages, it can give you far more control over when and how you refinance.

What Is Mortgage Laddering (Split or Multi-Part Loans)?

Mortgage laddering, sometimes called a split loan structure, means dividing your total mortgage into several “rungs”, each with its own term, rate type, or repayment schedule. For example:

$250k fixed for 1 year

$150k fixed for 3 years

$100k floating

This structure spreads your exposure across different rate periods, reducing the risk that all of your loan renews at once when market rates are unfavourable. Many NZ banks already support this approach — Westpac’s Split Home Loan is one example — but it can also be custom-built with your broker to suit your goals and appetite for flexibility.

Related reading: “Fixed vs Floating Mortgage NZ: Which Is Right for You”

Why Use This Strategy (and When It Works Best)

Mortgage laddering shines when rates are uncertain — which, in the current environment, is almost always.

Benefits include:

Reducing rate risk: You’re not locked into one rate or term. If rates drop, part of your loan can be refinanced sooner; if they rise, part of your loan stays protected.

Building flexibility: Each maturity date is a chance to adjust, pay down, or restructure a portion of your loan.

Accessing features: You can keep one portion fixed for security and another floating for making extra repayments or top-ups.

Smoothing renewals: Instead of facing one massive refinancing event, you’ll have staggered renewal dates, reducing risk and stress.

Ideal for:Borrowers with medium to large loans.

Homeowners expecting rate fluctuations or life changes (move, renovation, new job).

Those wanting a balance between certainty and flexibility.

Read more about “When and Why You Should Refinance Your NZ Mortgage”

How to Use Mortgage Laddering: Step-by-Step

Assess your current position: Know your loan balance, fixed terms, and when they expire.

Decide how many “rungs” you want: Typically 2–4 parts.

Allocate amounts: e.g., 40% / 30% / 30% or evenly split.

Choose term lengths:

Part A: 1-year fixed or floating

Part B: 2-year fixed

Part C: 5-year fixed

Select repayment profiles: One part could have faster repayments; another might use an offset or redraw facility.

Review at each maturity: When a portion expires, you can refinance, repay, or restructure based on market rates.

Track it carefully: Keep reminders for each part’s renewal date — losing track could mean missing an opportunity to refix at a better rate.

Tip: Combine this with our “Refinancing Strategy: How to Optimise in a Falling-Rate Environment” guide for the best results.

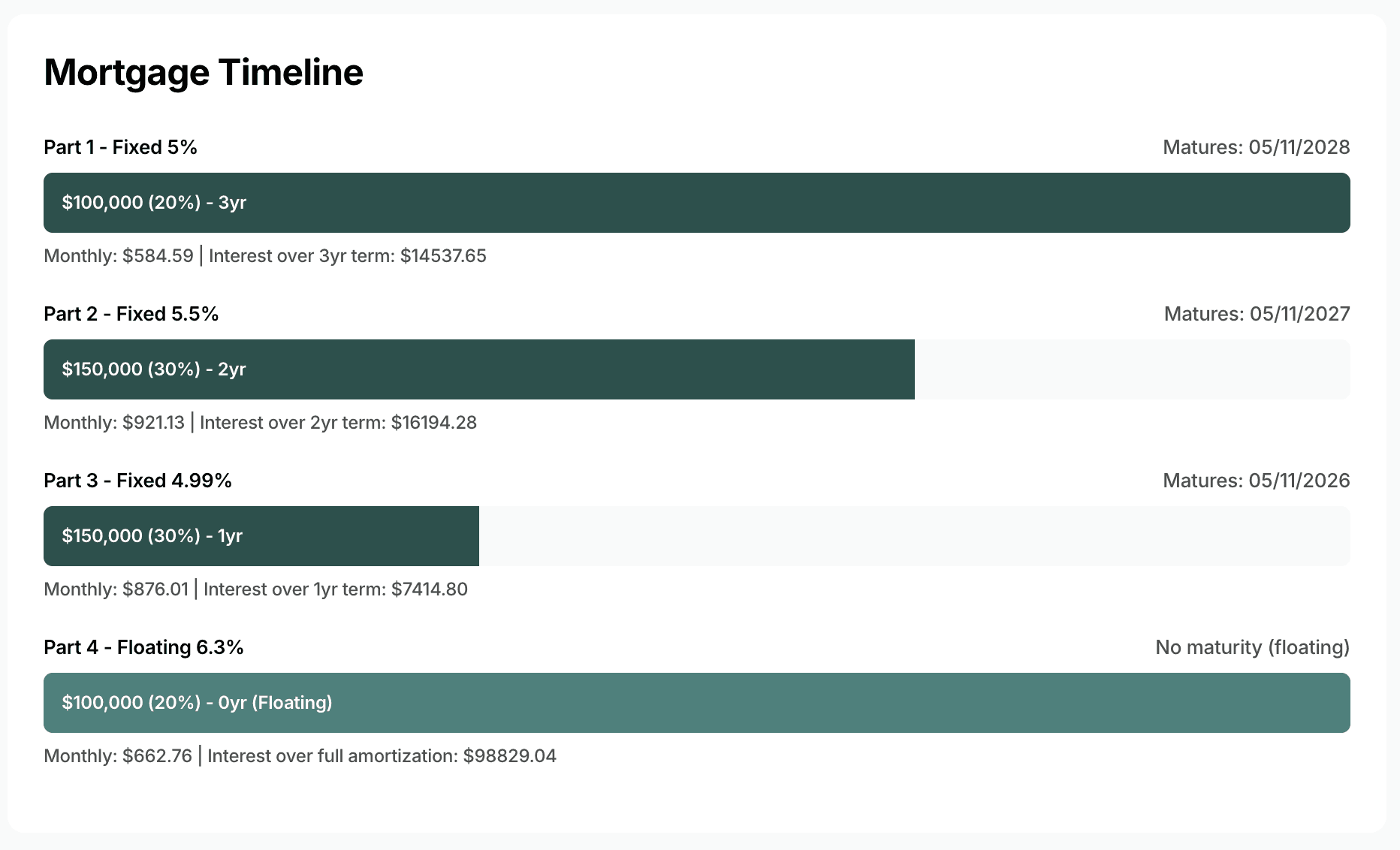

Real-World Example: How Laddering Works in Practice

Imagine a $600,000 home loan:

$200,000 fixed for 1 year at 4.49%

$200,000 fixed for 3 years at 4.75%

$200,000 fixed for 5 years at 4.99%

Over the next five years, each component rolls off at a different time. As the 1-year portion expires, you can refix at the new market rate, potentially lower, while the rest remains locked in. This smooths the risk of refixing everything when rates are high and gives you rolling opportunities to capture future rate drops.

If interest rates fall by 0.5% in the next year, you’ll immediately benefit from the lower rate on that first portion without having to break the rest of your mortgage.

Benefits and Risks to Keep in Mind

Benefits:

Greater flexibility to adjust or refinance.

Balanced exposure to rate movements.

Ability to make extra repayments on the floating portion.

Reduced refinancing risk across the whole loan.

Risks:More complexity — multiple parts mean multiple renewal dates.

Potential for multiple break fees if you sell or refinance mid-term.

Some banks may charge for added structure complexity.

If rates fall sharply, you may be stuck with part of your loan on a higher rate.

When to Consider Laddering (and When Not To)

Use laddering if:

You’re refinancing or approaching a fixed-rate expiry.

You expect rate volatility in the next 1–3 years.

You want flexibility for lump-sum payments, renovations, or a move.

Avoid laddering if:You prefer simplicity and don’t want to track multiple dates.

You plan to sell soon (break fees could outweigh benefits).

Practical Implementation Tips

Work with a mortgage adviser who understands multi-part loan setups.

Check with your bank about any structural fees or restrictions.

Build a calendar reminder system for each “rung.”

Revisit your structure annually — especially when rates shift significantly.

Use our interactive tools to simulate repayment outcomes and timing.

Try It Yourself: Our New Laddering & Refinance Calculators

Test your own loan setup using our new interactive tools:

Mortgage Laddering Simulator – model how splitting your loan changes repayments and total interest.

Refinancing Break-Even Calculator – see how long it takes to recover refinancing costs if you restructure part of your loan.

Both tools help you see, in real numbers, whether laddering makes sense for you — and how much flexibility you gain.

The Bottom Line

Mortgage laddering is a strategy built for real-world uncertainty. It’s not about predicting the next rate move — it’s about reducing exposure, creating options, and making your mortgage work smarter for you.

By dividing your home loan into multiple parts, you can protect against spikes, capture savings when rates fall, and plan each renewal strategically.

If you want to explore whether laddering is right for you, try our Mortgage Laddering Simulator or speak to our team. We’ll help you design a structure that fits your lifestyle, your goals, and the market cycle you’re in.

Contact us